Tutorial Categories

Last Updated: February 8, 2026 at 09:30

Bond Prices and Interest Rates: Understanding Why Prices Move

When you buy a bond, its future payments are fixed by contract—but its market price can still change every day. This tutorial explains why that happens. You’ll see why bond prices move in the opposite direction to interest rates, what it means for a bond to trade at a premium, discount, or par, and why some bonds are much more “rate‑sensitive” than others. By the end, you’ll be able to connect any bond‑market move back to one idea: the present value of future cash flows.

Introduction: The Fixed Promise in a Changing World

In the previous tutorial, we looked at the structure of a bond—its face value, coupon, and maturity date. Take a simple example: the “Neptune City 5% bond” that promises to pay $50 every year for ten years and $1,000 at the end. From the bondholder’s point of view, that cash flow calendar is fixed and predictable.

But the world around the bond is not fixed. Market interest rates—the return investors can get on new bonds with similar risk and maturity—change all the time. A bond that looked fair yesterday can suddenly look too generous or too stingy compared with newly issued bonds. The market solves this by adjusting the price of existing bonds, so their overall return stays in line with current rates. Understanding that adjustment is the key to understanding bond price behaviour.

Part 1: Bond Prices and Interest Rates – An Intuitive Analogy

Think of a bond like a voucher for one free coffee every day for a year. You are allowed to sell this voucher to someone else.

Scenario A: “Rates” Fall (Coffee gets more expensive)

- Suppose coffee prices at nearby shops rise from $5 to $7. Your voucher still buys a $7 coffee every day at no cost to the holder. That deal is now very attractive. People are willing to pay more than they would have before, because the voucher saves them more money each day.

Scenario B: “Rates” Rise (Coffee gets cheaper)

- Now imagine a new chain opens and starts selling coffee for $3. Your voucher, which effectively gives someone a $5 coffee, is no longer special. To convince someone to buy it, you must sell it for less than before, or they’ll just buy the cheaper coffee directly.

In this analogy:

- The coffee you get each day is like the bond’s coupon payment.

- The market coffee price is like the current interest rate in the bond market.

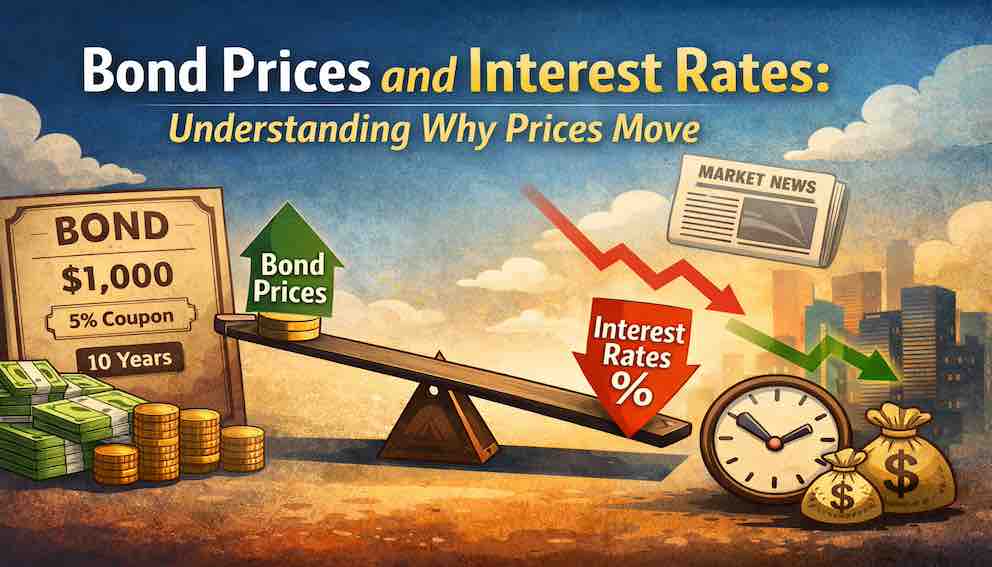

When market interest rates fall, existing bonds with higher coupons become more valuable, so their prices rise. When market rates rise, those same fixed coupons become less impressive, so bond prices fall.

Core rule:

Bond prices move in the opposite direction to interest rates.

Rates up → prices down.

Rates down → prices up.

Part 2: Premium, Par, and Discount – The Three States of a Bond

Because of that inverse relationship, a bond’s market price, compared with its face value, falls into three simple categories:

At a discount (Price below face value)

- The bond’s coupon rate is lower than the current market rate. To make the bond attractive, its price must drop so that the overall return matches what new bonds are paying.

- Example:

- Neptune City 5% bond (pays $50 per year on $1,000).

- New bonds of similar risk now pay 7%.

- To compete with 7%, the Neptune bond might trade at about $920 rather than $1,000.

At par (Price equals face value)

- The bond’s coupon rate is equal to the current market rate. In that case, price = face value, and the return you get from coupons plus principal is perfectly in line with the market.

At a premium (Price above face value)

- The bond’s coupon rate is higher than the current market rate. Investors are willing to pay more upfront to lock in those higher coupon payments.

- Example:

- New bonds of similar risk now pay only 3%.

- Your Neptune City 5% bond is generous by comparison.

- Its price might rise to about $1,150.

These price changes are not random. They simply ensure that, once you combine what you pay today with the cash you’ll receive later, the overall return is competitive with what the market currently offers.

Part 3: Discounting – How the Market Sets the Price

So how does the market arrive at those specific prices—$920, $1,000, $1,150? Conceptually, it uses discounting: turning future payments into their value today using the current interest rate.

Let’s simplify the Neptune City 5% bond to a 3‑year example:

- Face value: $1,000

- Coupon: 5% → $50 per year

- Maturity: 3 years

- Cash flows:

- Year 1: $50

- Year 2: $50

- Year 3: $50 + $1,000 = $1,050

Scenario 1: Market rate = 5% (Bond trades at par)

If the market rate is 5%, this bond is “fair”:

- Year 1: $50 ÷ 1.05 ≈ $47.62

- Year 2: $50 ÷ 1.05² ≈ $45.35

- Year 3: $1,050 ÷ 1.05³ ≈ $907.03

Add them up: about $1,000.

So the fair price is $1,000—trading at par.

Scenario 2: Market rate rises to 7% (Bond trades at a discount)

Now similar new bonds pay 7%:

- Year 1: $50 ÷ 1.07 ≈ $46.73

- Year 2: $50 ÷ 1.07² ≈ $43.65

- Year 3: $1,050 ÷ 1.07³ ≈ $829.62

Total: about $920.

The fair price falls to $920—a discount.

Scenario 3: Market rate falls to 3% (Bond trades at a premium)

Now similar new bonds pay only 3%:

- Year 1: $50 ÷ 1.03 ≈ $48.54

- Year 2: $50 ÷ 1.03² ≈ $47.14

- Year 3: $1,050 ÷ 1.03³ ≈ $1,053.90

Total: about $1,150.

The fair price rises to $1,150—a premium.

Key idea:

The bond’s cash flows didn’t change at all. Only the discount rate (the market interest rate) changed, and the present value moved with it. The market is constantly doing this present‑value calculation in the background; price is just the number that makes the bond’s return line up with current rates.

You don’t have to do these calculations by hand in real life, but knowing what’s happening under the hood explains why prices move.

Part 4: Why Some Bonds Are More “Sensitive” to Rates

All bonds are affected by interest rate changes, but some move a lot more than others. Two features matter most:

- Time to maturity

- Coupon size

1. Time to Maturity

The farther away a payment is, the more its value today depends on the interest rate you use to discount it.

Long‑term bonds

- Most of their value is in payments far in the future. A small change in rates is applied over many years, which has a big effect on today’s value. So long‑term bond prices can swing sharply when rates move.

Short‑term bonds

- Most of their payments happen soon. There is less time for discounting to magnify the effect of a rate change. So short‑term bond prices move less when rates change.

2. Coupon Size

Where is the bond’s value concentrated—spread out in coupons, or stacked in the final principal payment?

Low‑coupon bonds

- Pay relatively little interest along the way, so most of the value sits in the final principal repayment. That big payment far in the future is very sensitive to the discount rate. Result: low‑coupon bonds are more volatile.

High‑coupon bonds

- Pay more interest early and often. A larger share of their value comes from nearer‑term payments, which are less sensitive to rate changes. Result: high‑coupon bonds tend to be more stable.

Structure also matters (bullet vs. amortizing)

- Bullet bonds return all principal at once at maturity, which concentrates risk in one distant payment and increases rate sensitivity.

- Amortizing bonds repay principal gradually, bringing some of that value closer to today and slightly reducing rate sensitivity.

Rule of thumb:

- Most sensitive: long‑term, low‑coupon, bullet bonds.

- Least sensitive: short‑term, high‑coupon, amortizing bonds.

Part 5: Applying the Model – Reading Market Moves

Once you understand the price–rate see‑saw and discounting, headlines start to make sense.

Headline: “Central bank raises interest rates, bond prices fall.”

- New bonds now offer higher coupons.

- Existing bonds with lower coupons are less attractive unless their prices drop.

- Prices fall most for long‑term, low‑coupon bonds.

Headline: “Investors rush into safe government bonds, yields drop.”

- Strong demand pushes bond prices up.

- When price goes up for a fixed set of cash flows, the yield (the implied return) goes down.

Your bond fund falls in value:

- This usually means rates have risen since the fund bought many of its bonds.

- The underlying bonds still pay the same coupons and principal, but their market prices have adjusted to the new, higher‑rate environment.

Instead of feeling like mysterious volatility, these moves become the predictable outcome of the same mechanism: changing discount rates applied to fixed cash flows.

Important note about bond prices

So far, we’ve focused on how changes in market interest rates push bond prices up or down, but rates are not the only force at work. Investors also change what they are willing to pay based on credit risk (how safe the issuer looks), simple demand and supply (how many buyers or sellers are in the market), and shifts in inflation expectations or overall risk appetite. A downgrade in a company’s credit rating, a wave of forced selling by funds, or a sudden “flight to safety” into government bonds can all move prices even if official interest rates stay unchanged. In other words, bond prices reflect not just math about discounting cash flows, but also the market’s evolving views on risk, safety, and scarcity.

Conclusion: Mastering the Bond Price See‑Saw

You now have the core mental model for bond price behaviour:

- Price and yield are a see‑saw. For a given set of cash flows, when price goes up, yield goes down; when price goes down, yield goes up.

- Market rates are the anchor. Bond prices adjust so that each bond’s overall return stays competitive with current interest rates.

- Structure drives sensitivity. Longer maturities, lower coupons, and bullet structures make bonds more sensitive to rate changes; shorter maturities, higher coupons, and amortizing structures make them less sensitive.

- Discounting ties it all together. Price is simply the present value of all future payments using today’s required return.

With this framework, bonds stop being static pieces of paper and become living instruments whose prices reflect the market’s constantly updated view of time and risk. In the next tutorial, we’ll formalize this idea of “sensitivity” by introducing Duration—the standard tool for measuring how much a bond’s price is likely to move when interest rates change.

About Swati Sharma

Lead Editor at MyEyze, Economist & Finance Research WriterSwati Sharma is an economist with a Bachelor’s degree in Economics (Honours), CIPD Level 5 certification, and an MBA, and over 18 years of experience across management consulting, investment, and technology organizations. She specializes in research-driven financial education, focusing on economics, markets, and investor behavior, with a passion for making complex financial concepts clear, accurate, and accessible to a broad audience.

Disclaimer

This article is for educational purposes only and should not be interpreted as financial advice. Readers should consult a qualified financial professional before making investment decisions. Assistance from AI-powered generative tools was taken to format and improve language flow. While we strive for accuracy, this content may contain errors or omissions and should be independently verified.